Being stuck in the middle class is a common experience for many young and middle-aged Indians. While it’s a comfortable position compared to lower income groups, many aspire for the financial independence and security that come with moving beyond this stage. Breaking free from the middle-class trap requires a mix of smart financial planning, education, and strategic lifestyle changes and of course saving money.

If you are stuck in the middle-class trap and wondering how to break free and become financially free over a period of time, then we have got you covered. Today in this post, we are decoding the Indian middle-class trap and sharing actionable steps to help you come out of this trap and become financially free.

But, before we dive in, let’s understand the middle-class trap first.

What is the Indian Middle Class Trap?

The Indian middle-class trap is a common financial phenomenon where, despite an increase in income, people find themselves unable to save or invest significantly, making it difficult to secure their financial future.

This situation often occurs due to a few key factors, such as:

1. Lifestyle Inflation

As income increases, so do expenses. People tend to upgrade their lifestyle, purchasing more expensive items, dining out more frequently, and spending more on non-essential luxuries. This increase in spending can absorb any additional income, leaving little or no room for savings and investments.

Example: When someone receives a salary hike, they might move to a bigger apartment, buy a new car, or spend more on vacations. While these upgrades provide immediate satisfaction, they also significantly increase monthly expenses.

2. Rising Costs of Living

The cost of living in urban areas is continually rising, with higher prices for housing, education, healthcare, and other essential services. This escalation can outpace income growth, making it challenging to save.

Example: Tuition fees for quality education and healthcare costs are escalating, putting additional financial pressure on middle-class families.

3. Debt and Loans

Many middle-class individuals rely on loans and credit to fund their lifestyle. While taking loans for necessary expenses like housing and education is common, high-interest consumer debt such as credit card debt can be particularly damaging. The interest payments on these debts can consume a significant portion of income, reducing the ability to save and invest.

Example: A significant portion of monthly income might go towards EMI payments for home loans, car loans, or personal loans, leaving less money available for savings or investments.

4. Lack of Financial Planning

Many people do not engage in effective financial planning. Without a clear plan, it’s easy to lose track of expenses and miss opportunities to save and invest wisely. Effective financial planning involves budgeting, setting financial goals, and regularly reviewing and adjusting financial strategies.

Example: Without a budget, people may spend impulsively and fail to allocate funds for important financial goals such as retirement, emergency funds, or children’s education.

5. Cultural and Social Pressures

In India, cultural and social expectations often influence spending habits. Events such as weddings, festivals, and social gatherings can lead to significant expenditures. Additionally, there can be pressure to maintain a certain lifestyle to match societal standards, leading to further financial strain.

Example: Spending lavishly on weddings or festivals due to societal expectations can drain savings and increase financial pressure.

Strategies for Coming Out of the Middle Class Trap

Understanding these factors is the first step toward breaking free from the middle-class trap. By recognizing the impact of lifestyle inflation, rising costs, debt, lack of financial planning, and social pressures, you can take actionable steps to manage your finances better.

The key is to create a balance where your income growth translates into real financial security and freedom, rather than just increased expenses.

1. Understand Your Finances

The first step to financial freedom is understanding where your money goes. Track your monthly income and expenses minutely. And when you track your expenses, you will be able to see where you can save some money every month. Use budgeting apps like Walnut or Money Manager to help keep your finances in check.

2. Invest Wisely

Instead of letting your savings sit idle in a savings bank account, consider investing in assets that grow over time.

Here are a few options you may like to consider:

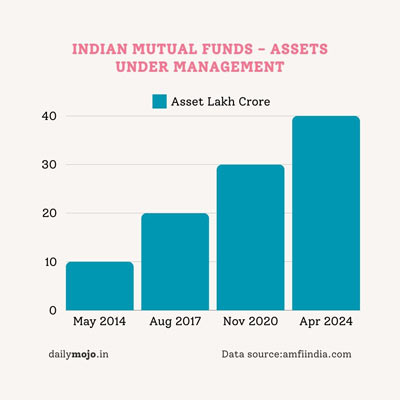

Mutual Funds: These are professionally managed investment funds that pool money from many investors to purchase securities. They offer higher returns than traditional savings accounts.

Stat Alert: According to the Association of Mutual Funds in India (AMFI), the mutual fund industry has grown by over 20% in the past five years.

Stock Market: Investing in stocks can be risky, but with proper research and a long-term perspective, it can yield significant returns.

Real Estate: Property investments can provide rental income and appreciate over time.

3. Increase Your Earning Potential

Upgrade Your Skills: In today’s competitive job market, having additional skills can give you an edge. Platforms like Coursera, Udemy, and Skillshare offer affordable courses on various subjects.

A survey by LinkedIn showed that professionals who continually upskill earn 10-15% more than those who don’t.

Side Hustles: Consider starting a side business or freelance work. This not only provides additional income but also helps you explore your passions.

4. Avoid Lifestyle Inflation

As your income increases, it’s tempting to upgrade your lifestyle. However, this can trap you in a cycle of living paycheck to paycheck. Practice frugality by:

Living Below Your Means: Just because you earn more doesn’t mean you should spend more. Focus on saving and investing the extra income.

According to the Reserve Bank of India (RBI), the savings rate in India has been declining, indicating that people are spending more rather than saving.

Smart Shopping: Look for discounts, use cashback apps, and avoid impulsive buying. This can help you save a significant amount over time.

5. Plan for the Future

Emergency Fund: Ensure you have at least 6-12 months of living expenses saved up for emergencies. This fund will provide a safety net during unexpected financial challenges.

Retirement Planning: Start saving for retirement early. Consider investing in Provident Fund (PF), Public Provident Fund (PPF), or National Pension System (NPS).

According to a survey by the Economic Times, only 33% of Indians are confident about their retirement savings.

6. Manage Debt Wisely

Avoid Unnecessary Loans: Only take loans when absolutely necessary. High-interest loans can cripple your finances.

Pay Off Debts Early: If you have existing loans, try to pay them off as soon as possible. This will save you money on interest payments.

7. Stay Informed and Adapt

The financial landscape is always changing. Stay updated with the latest trends and adapt your strategies accordingly. Read financial news, follow expert blogs, and attend webinars.

Conclusion

Breaking out of the Indian middle-class trap is not about making drastic changes overnight but about making consistent, smart financial decisions over time. By understanding your finances, investing wisely, increasing your earning potential, avoiding lifestyle inflation, planning for the future, managing debt, and staying informed, you can pave the way to financial independence and security.

Remember, every small step you take today can lead to significant financial growth in the future.

Stay committed, be patient, and watch your financial dreams turn into reality.